|Table of Contents|

|

|

1. Preferential Land Value Increment Tax Rate: Once in a Lifetime and One House per Lifetime

|

|

Once in a lifetime

|

One house per lifetime

|

|---|---|---|

|

Difference

|

|

|

|

Area

|

Urban land: not more than 3 ares

non-urban land: not more than 7 ares

|

Urban land: not more than 1.5 ares

non-urban land: not more than 3.5 ares |

|

Tax Rate

|

10%,

while the general tax rate is 20%–40% |

|

|

Number of Uses

|

Only once in a lifetime

|

假日價No limit on the number of uses

(Provided that all applicable requirements are met.) |

|

Notes

|

|

|

2. What Is “Once in a Lifetime”?

“Once in a lifetime” means that a person has only one opportunity in their lifetime to apply to pay land value increment tax at the self-use residential tax rate of 10%, provided that the following requirements are met:

- The owner of the building on the land must be the landowner, the landowner’s spouse, or a lineal relative.

- The landowner, the landowner’s spouse, or a lineal relative must have completed household registration before signing the sale and purchase contract.

- The property must not have been rented out or used for business within one year before the sale.

- If the self-use residential building was completed less than one year ago, the assessed present value of the house must be at least 10% of the publicly announced current land value of the house site.

- Urban land must not exceed 3 ares, approximately 90.75 ping; non-urban land must not exceed 7 ares, approximately 211.75 ping.

3. What Is “One House per Lifetime”?

“One house per lifetime” means that, on the premise that the “once in a lifetime” preferential rate has already been used, a landowner who owns only one house at the time of sale and meets the following requirements may apply to pay land value increment tax at the self-use residential tax rate of 10%:

-

At the time of sale, the landowner, the landowner’s spouse, and the landowner’s minor children must not own any house other than the self-use residential property being sold.

-

The landowner must have held the land for more than six years before the sale.

-

Before the land is sold, the landowner, the landowner’s spouse, or the landowner’s minor children must have household registration at the property, and the self-use residential property must have been held continuously for at least six years.

-

The property must not have been used for business or rented out within five years before the sale

-

Area limits: urban land must not exceed 1.5 ares, approximately 45.375 ping; non-urban land must not exceed 3.5 ares, approximately 105.875 ping.

.jpg)

▲ Receiving this official letter after filing the application means that the application has been approved.

4. How to Apply for “Once in a Lifetime” and “One House per Lifetime”

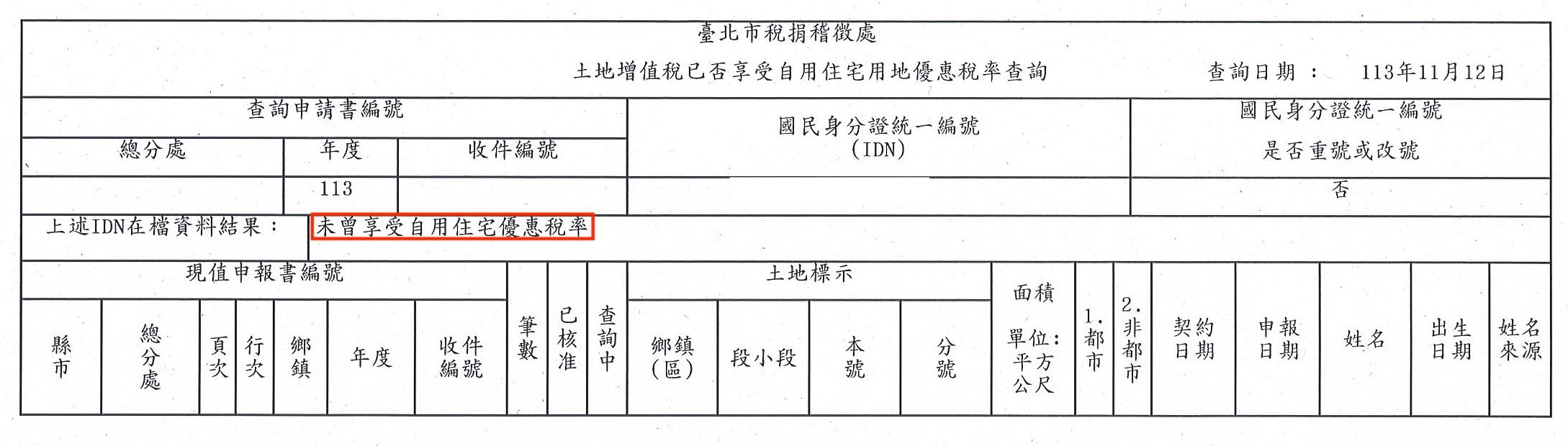

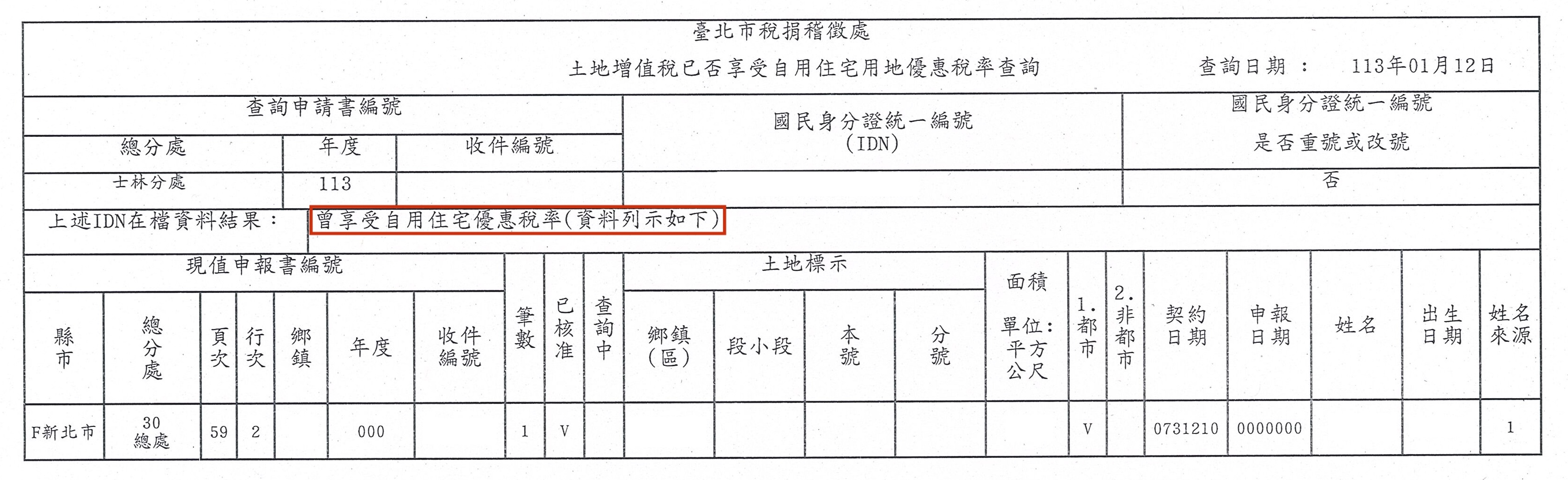

A. How to Check Whether the “Once in a Lifetime” Preferential Tax Rate Has Been Used

-

Online inquiry: Prepare your Citizen Digital Certificate or National Health Insurance card, and use the online inquiry system on the Ministry of Finance Taxation Portal.

-

In-person application: Bring the original national ID card to the “full-function service counter” at any tax collection office in Taiwan. If the application is handled by an agent, a power of attorney, a copy of the landowner’s national ID card, and the agent’s original national ID card must be prepared.

B. Required Documents for Application

-

Application form: Application for Land Sold to Be Taxed at the Self-Use Residential Land Tax Rate

-

Transfer contract: Copy of the land ownership transfer contract, which is the official standard contract

-

No-lease declaration: Declaration by the landowner stating that there is no lease relationship

-

Building proof: Documents proving the building improvement, such as the building survey result map or the building improvement inspection result notice

-

Household registration proof: Declaration by the household-registered person stating that there is no lease relationship, or declaration by the household-registered person stating that there is a lease relationship together with a copy of their national ID card

C. Tax Authority Case Example

▲The “once in a lifetime” preferential rate has not yet been applied for, and the “one house per lifetime” preferential rate has not yet been used. The “once in a lifetime” preferential rate must have been applied for before the taxpayer becomes eligible to use the “one house per lifetime” preferential rate.

▲The “once in a lifetime” preferential rate has not yet been applied for, and the “one house per lifetime” preferential rate has not yet been used. The “once in a lifetime” preferential rate must have been applied for before the taxpayer becomes eligible to use the “one house per lifetime” preferential rate.

5. Key Reminders

-

The “once in a lifetime” preferential rate can only be used once. By contrast, “one house per lifetime” may be used multiple times if the applicable requirements are met. However, the “once in a lifetime” preferential rate must have been used before the taxpayer becomes eligible to use “one house per lifetime.”

-

The requirements for “one house per lifetime” are stricter, but it may be used more than once.

-

Whether it is “once in a lifetime” or “one house per lifetime,” the preferential rate applies only to sale transactions. Gift transfers are governed by different rules. In addition, this is unrelated to whether house tax or land value tax applies the self-use residential tax rate, because the applicable requirements for land value increment tax are different from those two taxes.

6. Supplementary Explanation: What Is Land Value Increment Tax?

Land value increment tax is a tax imposed in Taiwan when land ownership is transferred. It is calculated based on the increase in the publicly announced current land value and the length of time the land has been held.

-

|Formula for Total Land Value Increment[1]

-

Total land value increment = land sale proceeds − costs spent on the land

-

Costs spent on the land include:

-

Land improvement costs, such as soil replacement or land filling.

-

Engineering benefit charges.

-

Land readjustment burden costs.

-

The publicly announced current land value of land donated without compensation as land for public facilities due to a change in land use.

-

-

-

| Progressive Tax Rates Based on the Multiple of Land Value Increment[2]

-

Similar to how general income tax rates are determined, land value increment tax also adopts a progressive tax rate system. The greater the increase in land value, the higher the applicable tax bracket. Land value increment tax is divided into three brackets based on the multiple of land value increment, namely 20%, 30%, and 40%. For self-use residential land, the tax rate is fixed at 10%.

-

|

Land Value Increment Tax Rate Standards

|

|

|---|---|

|

Range Exceeding the Original Prescribed Land Value or the Previous Transfer Value

|

Applicable Tax Rate for the Excess Portion

|

|

Self-Use Residential Property

|

假日價10%

|

|

Less than 100%

|

假日價20%

|

|

100% ≤ Excess Portion < 200%

|

假日價30%

|

|

Excess Portion ≥ 200%

|

假日價40%

|

-

The increase in value is defined as the portion by which the land value exceeds the original prescribed land value or the current value at the previous transfer. The “excess” portion will be subject to the corresponding tax rate based on the extent of the increase.

-

However, land value increment tax may also be reduced based on the length of time the land has been held. The longer the holding period, the higher the reduction percentage. The reduction rates are shown in the table below:

|

Land Value Increment Tax Reduction Standards

|

|

|---|---|

|

Holding Period

|

Reduction Rate

|

|

Less than 20 years

|

X

|

|

20 years ≤ Holding Period < 30 years

|

假日價20%

|

|

30 years ≤ Holding Period < 40 years

|

假日價30%

|

|

Holding Period ≥ 40 years

|

假日價40%

|

-

| Land Value Increment Tax Formula(=[1]X[2])

-

Land value increment tax = (total land value increment × tax rate) − (progressive difference + long-term holding reduction + additional land value tax paid + legally applicable tax reductions)

-

.png)