As the government has increased restrictions on property hoarding and mortgage lending, many people have turned to gifts between spouses as a way to allocate assets. If the legal tool of “spousal gifts” is used properly to transfer property, it can indeed achieve a tax-free legal effect in certain respects.

1. Tax-Exempt Items, Fees, and Whether Spousal Gifts Must Be Reported to the National Taxation Bureau

-

Gift tax: not included in the total amount of gifts

-

According to Article 20, Paragraph 1, Subparagraph 6 of the Estate and Gift Tax Act, property gifted between spouses is not included in the total amount of gifts.

-

In other words, gifts between spouses are not subject to gift tax regardless of the amount.

-

Land value increment tax: non-imposition may be applied for

-

According to Article 28-2 of the Land Tax Act, for land gifted between spouses, the parties may apply for non-imposition of land value increment tax.

-

The non-imposition of land value increment tax for gifts between spouses is not the same as an exemption. It only means that land value increment tax is temporarily not imposed for the period during which the donor held the property. The tax payment is merely deferred. Therefore, when the donee later sells the real estate, the land value increment tax that was not paid for the donor’s holding period must still be paid together with the tax arising at that time.

-

When the property is later transferred to a third party, the total land value increment for the entire holding period of both spouses, even if they have divorced, must still be combined for land value increment tax purposes. The original prescribed land value before the first gift of the land will still be used as the original land value for calculating land value increment tax.

-

Note: deed tax, stamp tax, and land administration registration fees still have to be paid.

-

Deed tax is 6% of the assessed present value of the house. Generally, newer houses and properties in better locations tend to have a higher assessed present value.

-

- Do gifts between spouses need to be reported? ★

-

Yes. Gifts of movable property must also be reported in accordance with the law.

-

However, under Article 45 of the Estate and Gift Tax Act, underreporting or failure to report is subject to a fine of up to two times the amount of tax omitted. Since gifts between spouses generally do not result in gift tax payable, in practice many people choose not to file a gift tax report. Even if the omission is discovered, no fine will arise if there is no omitted tax amount.

-

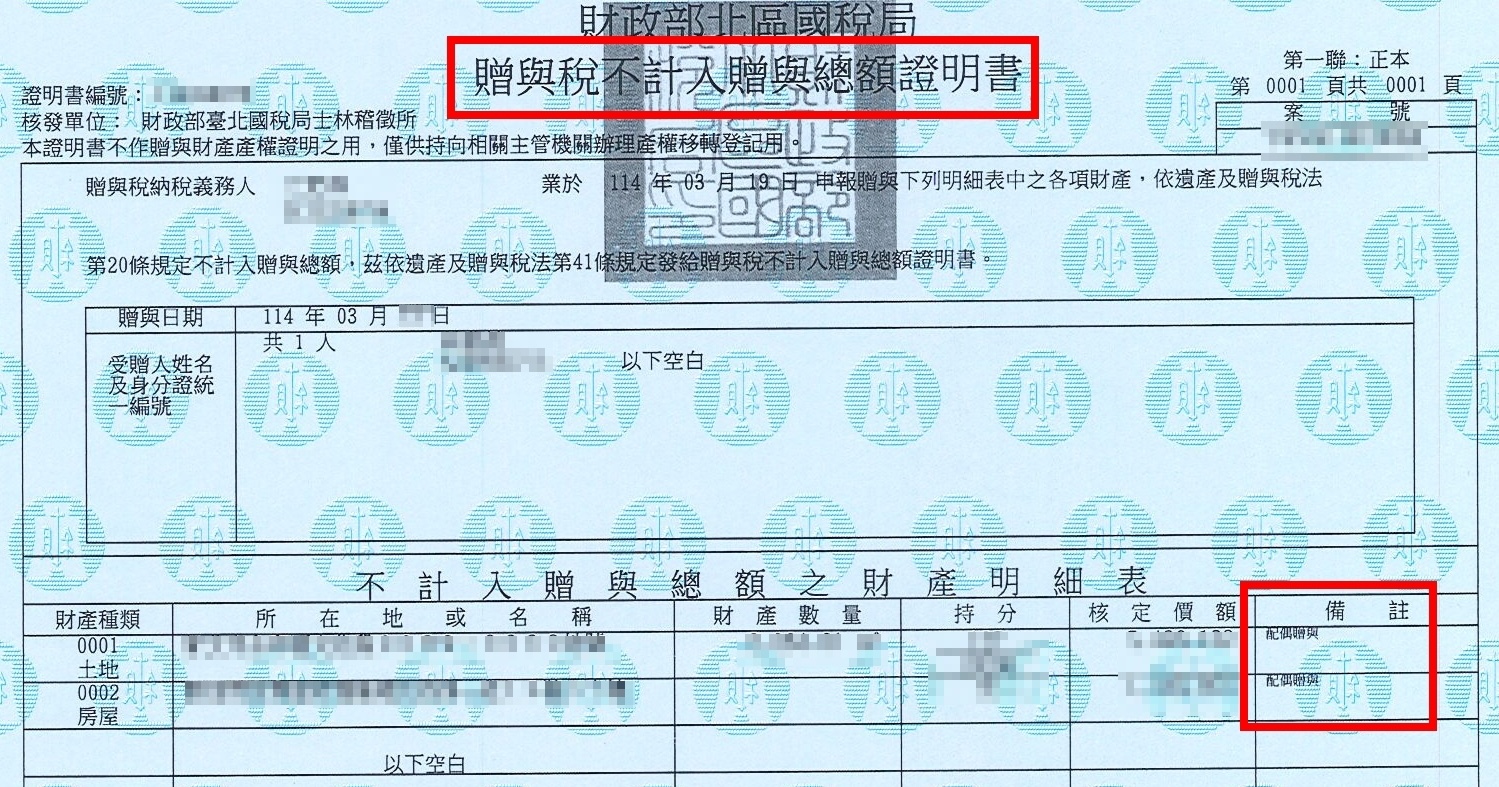

However, an exception may arise if a later transaction involves a sale between relatives within the second degree of kinship. For example, if the wife gives cash to the husband, and the husband then purchases a house from his father-in-law, the National Taxation Bureau may still require the husband to provide proof of the source of funds. In other words, a certificate stating that the gift tax is not included in the total amount of gifts may still need to be provided.

-

If the gift involves real estate, gift tax must be reported to the National Taxation Bureau, and a “certificate stating that the gift is not included in the total amount of gifts” must be obtained before the real estate can be transferred.

-

Next, let us look at the common practical purposes of gifts between spouses. These may include balancing the assets held by both spouses to achieve tax savings, arranging financial planning for passing assets to children, or providing financial security for each other. So what are the benefits of gifts between spouses?

2. Benefits of Gifts Between Spouses and Tax Planning Uses

-

Managing Future Mortgage Loan-to-Value Limits and First-Time Homebuyer Benefits

-

To curb housing prices and investment-driven home purchases, the government and banks currently impose loan-to-value ratio limits on second-home purchases, while offering various mortgage benefits to first-time homebuyers.

-

The actual definition of a first-time homebuyer is that the borrower does not own any residential property under their name. In other words, as long as no residential property is registered under the borrower’s name, the borrower may qualify to apply for a first-time homebuyer mortgage.

-

Therefore, a gift between spouses may be used to transfer real estate from one spouse to the other, allowing the transferring spouse to still qualify for general mortgage programs.

-

Asset Allocation

-

According to Article 20, Paragraph 1, Subparagraph 6 of the Estate and Gift Tax Act, property gifted between spouses is not included in the total amount of gifts.

-

In other words, gifts between spouses are not subject to gift tax and will not use up each person’s annual NT$2.44 million gift tax exemption.

-

For example, if a father wants to gift NT$4.8 million to his son, the amount exceeds the annual exemption. The husband may first use the rule that gifts between spouses are not included in the total amount of gifts and gift NT$2.4 million to his spouse. Then the husband and wife may each gift NT$2.4 million to the same son at the same time.

-

If the total value of property gifted by either the husband or wife to others within the same year is no more than NT$2.44 million, gift tax will not be imposed. This allows both spouses to make separate gifts to the child within one year, shortening the time needed to complete the gifting plan.

-

Important Supplement:

-

According to Article 15 of the Estate and Gift Tax Act, property gifted to a spouse within two years before the decedent’s death shall be deemed part of the decedent’s estate and included in the estate for estate tax assessment.

-

Want to know how to save taxes through distribution of the difference in marital remaining property? Distribution of the difference in marital remaining property is a powerful legal tax-saving tool.

-

If property was gifted between spouses within two years before death, it must be added back when calculating the total estate. This is because the National Taxation Bureau does not want people to avoid estate tax by gifting away all property when they know they may soon pass away.

-

If you are seriously ill and wish to gift specific property to your spouse during your lifetime so that it does not become estate property, which would otherwise give other heirs statutory shares or, even with a will, compulsory portions, then when making a lifetime gift between spouses, you must also consider the rule that gifts made within two years before death will be included in the total estate for estate tax calculation.

-

-

Tax Planning: Using the Once-in-a-Lifetime Preferential Land Value Increment Tax Rate for Self-Use Residential Land

-

For example, suppose the husband is preparing to sell a house under his name and faces a high land value increment tax, but he has already used the once-in-a-lifetime preferential land value increment tax rate for self-use residential land. He may first gift the house to his wife and then sell it afterward.

-

If the spouse who owns the house has already used the once-in-a-lifetime preferential land value increment tax rate, while the other spouse has not yet used it, the house may be gifted to the spouse who has not used the preferential rate and then sold. As long as the requirements for the preferential land value increment tax rate for self-use residential land are met, the once-in-a-lifetime 10% tax rate may still apply.

3. Application Process for Real Estate Gifts Between Spouses

-

Prepare the required documents and affix the required seals.

-

File deed tax, land value increment tax, and stamp tax with the local tax office.

-

Pay the taxes after the tax bills are issued.

-

File gift tax with the National Taxation Bureau at the household registration location.

-

Check for any outstanding taxes with the local tax office.

-

Complete the ownership transfer registration with the land office.

4. Important Notes on Real Estate Gifts Between Spouses Under the New House and Land Transactions Income Tax System

After the new house and land transactions income tax system officially took effect on January 1, 2016, special attention must be paid to how income tax should be reported and calculated when real estate gifted between spouses is later sold. Whether the old or new system applies depends on the date when the spouse originally acquired the real estate before the gift.

-

How the Original Acquisition Date Affects Whether the Old or New Tax System Applies

-

If real estate is gifted between spouses and later sold, the applicable income tax system is determined based on the date when the spouse originally acquired the real estate before the gift. It is not determined by the date when the spousal gift was made

-

Example: A and B are spouses. A gifts real estate to B. B sells the real estate after January 1, 2016.

|

A’s Original Acquisition Date

|

ax System Applicable When B Sells

|

B之所得稅計算方式

|

|

Before January 1, 2016

|

Old system

|

Calculated based on the proportion of the assessed present value of the house under the standard assessment method, or based on the house-and-land ratio of actual profit under the actual assessment method

|

|

On or after January 1, 2016

|

New system, namely the house and land transactions income tax

|

Income is calculated based on the actual transaction price and costs

|

-

If the Spouse Originally Acquired the Real Estate on or After January 1, 2016, How Are the Donee Spouse’s Holding Period and Tax Rate Determined?

-

If the spouse originally acquired the real estate on or after January 1, 2016, and then gifts it to the other spouse, the house and land transactions income tax system will necessarily apply when the other spouse later sells the property.

-

When one spouse receives real estate as a gift from the other spouse, even if the gift occurs after the new system has taken effect, the holding period may still be determined based on the date when the donor spouse originally acquired the real estate, and the applicable tax rate is determined based on the original acquisition reason.

-

According to the National Taxation Bureau, under Article 14-4 of the Income Tax Act, when an individual sells a house and land acquired as a gift from a spouse, the acquisition date should be the original acquisition date of the house and land before the first mutual gift between the spouses. The holding period of the spouse may be combined in the calculation.

-

Example: A and B are spouses. A purchased a real estate property on January 1, 2016. A gifted the property to B on January 1, 2021. B sold the property on January 1, 2026. In this case, B’s holding period may include A’s holding period, for a total of 10 years. The applicable house and land transactions income tax rate is 15%.

-

Method of Determination:

|

Method of Gift

|

Determination of Holding Period

|

Applicable Tax Rate

|

|

Gift from a spouse

|

Determined based on the donor spouse’s original acquisition date

|

The applicable tax system is determined based on the donor spouse’s original acquisition date

|

|

Gift from a non-spouse

|

Calculated from the date the gift is received

|

The new tax system applies in all cases

|

★The spouse who receives real estate as a gift from the other spouse may enjoy the same rights as the spouse who originally acquired the property, and may choose the most favorable method between the old and new systems to calculate gains or losses from the real estate transaction.

This rule provides a certain degree of tax benefit for real estate gifts between spouses and gives couples greater flexibility in reasonably allocating property between them.

5. In Divorce, Real Estate May Be Transferred Through Distribution of the Difference in Marital Remaining Property

This rule provides a certain degree of tax benefit for real estate gifts between spouses and gives couples greater flexibility in reasonably allocating property between them.

5. In Divorce, Real Estate May Be Transferred Through Distribution of the Difference in Marital Remaining Property

-

If a couple is preparing for divorce, real estate may be allocated not only through a real estate gift between spouses, but also through distribution of the difference in marital remaining property under Article 1030-1 of the Civil Code, which may offer greater tax savings.

|

Tax or Fee Item

|

Real Estate Gift Between Spouses

|

Real Estate Transfer Through Distribution of the Difference in Marital Remaining Property — Better Option

|

|---|---|---|

|

Land value increment tax

|

X

|

假日價X

|

|

Gift tax

|

X

|

X

|

|

Deed tax on the house

|

V

|

假日價X

|

|

Stamp tax on the building

|

V

|

X

|

|

Stamp tax on the land

|

V

|

X

|

.png)